Introduction

Bayesian inference provides a principled framework for updating beliefs as new evidence arrives. In project risk management, this means starting with prior estimates of risk probability (based on historical data or expert judgment), then refining those estimates as on-site observations accumulate.

Bayes’ theorem states:

The PRA package provides four Bayesian functions organized into two stages:

| Stage | Function | Purpose |

|---|---|---|

| Prior | risk_prob() |

Compute risk probability from root causes (no observations yet) |

| Prior | cost_pdf() |

Sample prior cost distribution based on risk probabilities |

| Posterior | risk_post_prob() |

Update risk probability after observing cause status |

| Posterior | cost_post_pdf() |

Sample posterior cost distribution based on observed risks |

Step 1: Prior Risk Probability

Before any observations are made, risk_prob() computes

the probability of a risk event R occurring given two potential root

causes. For each cause, we supply:

-

cause_probs— prior probability that the cause is present -

risks_given_causes— P(R | cause present) -

risks_given_not_causes— P(R | cause absent)

prior_risk <- risk_prob(cause_probs, risks_given_causes, risks_given_not_causes)

cat("Prior probability of risk event R:", round(prior_risk, 3), "\n")Prior probability of risk event R: 0.82

Step 2: Prior Cost Distribution

Given the prior risk probabilities, cost_pdf() samples

the cost distribution before any field observations. Three independent

risk events can each contribute cost if they occur.

risk_probs <- c(0.3, 0.5, 0.2)

means_given_risks <- c(10000, 15000, 5000)

sds_given_risks <- c(2000, 1000, 1000)

base_cost <- 2000

prior_samples <- cost_pdf(

num_sims = 5000,

risk_probs = risk_probs,

means_given_risks = means_given_risks,

sds_given_risks = sds_given_risks,

base_cost = base_cost

)We will compare this to the posterior distribution in Step 4.

Step 3: Posterior Risk Probability (Bayesian Update)

After inspecting the project site, we observe that Cause 1 is present

(= 1). Cause 2 has not yet been assessed (= NA).

risk_post_prob() updates the risk probability using only

the available evidence — NA causes are treated as unobserved and do not

contribute to the update.

# C1 observed as present; C2 not yet assessed

observed_causes <- c(1, NA)

posterior_risk <- risk_post_prob(

cause_probs, risks_given_causes,

risks_given_not_causes, observed_causes

)

cat("Posterior probability of risk event R:", round(posterior_risk, 3), "\n")Posterior probability of risk event R: 0.632

Observing Cause 1 (which has a strong link to R) raises the risk probability substantially. The NA for Cause 2 is simply ignored — only confirmed observations drive the update.

Prior vs. Posterior Probability

prob_data <- data.frame(

Stage = c("Prior", "Posterior"),

Probability = c(prior_risk, posterior_risk)

)

p <- ggplot2::ggplot(prob_data, ggplot2::aes(x = Stage, y = Probability, fill = Stage)) +

ggplot2::geom_col(width = 0.5, show.legend = FALSE) +

ggplot2::geom_text(ggplot2::aes(label = round(Probability, 3)),

vjust = -0.4, size = 4.5

) +

ggplot2::scale_fill_manual(values = c("Prior" = "steelblue", "Posterior" = "tomato")) +

ggplot2::scale_y_continuous(limits = c(0, 1), labels = scales::percent) +

ggplot2::labs(

title = "Bayesian Update: Risk Probability",

x = NULL,

y = "P(Risk Event R)"

) +

ggplot2::theme_minimal(base_size = 13)

print(p)

The bar chart makes the Bayesian update tangible: observing Cause 1 nearly doubles the estimated probability of the risk event.

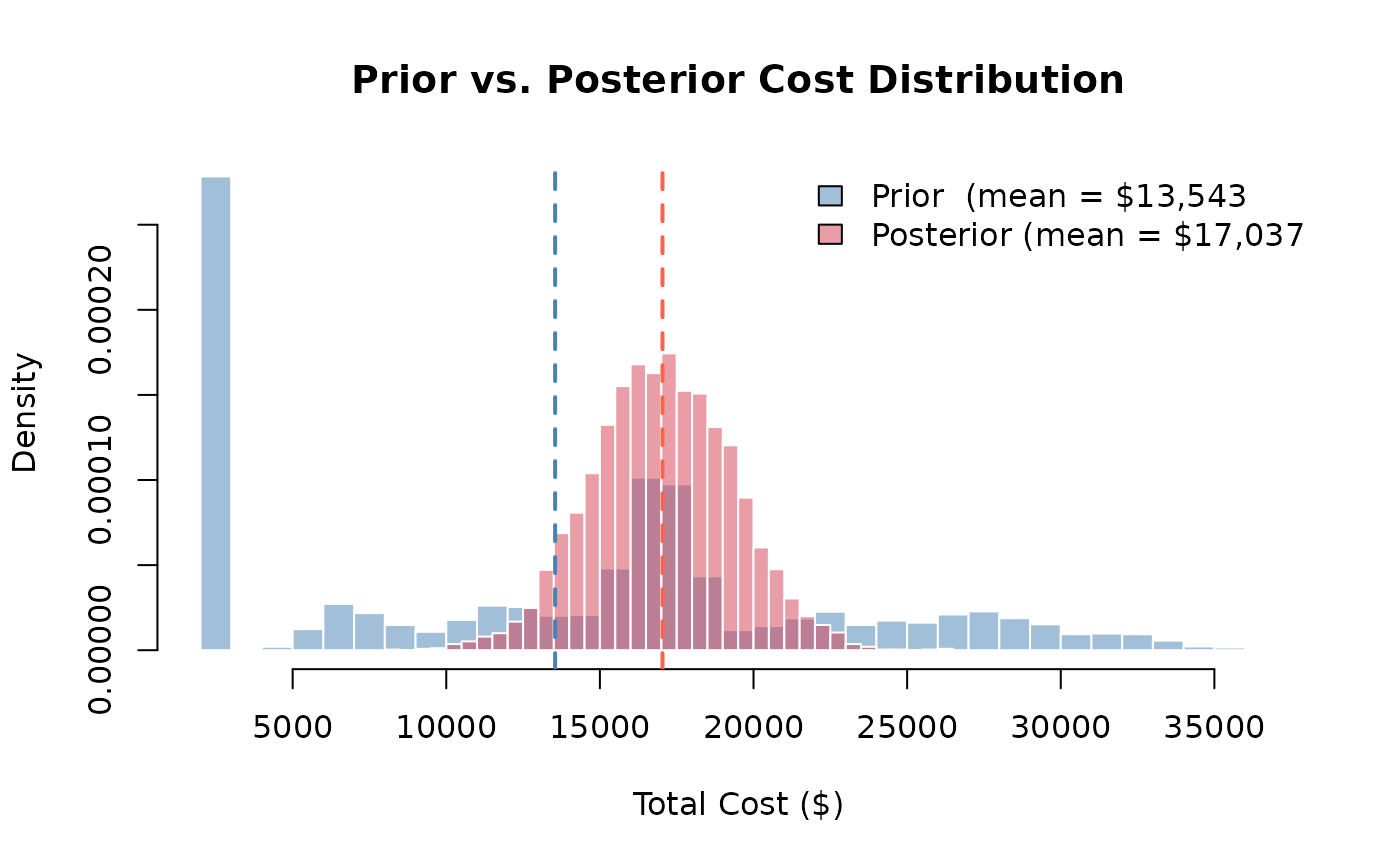

Step 4: Posterior Cost Distribution

Now that we know Cause 1 is present (Risk 1 occurs), and one risk

remains unobserved (Risk 2 = NA), cost_post_pdf() samples

the posterior cost distribution. Observed risks that occurred (= 1) add

their cost; unobserved risks (= NA) are excluded from the

simulation.

observed_risks <- c(1, NA, 1) # Risk 1 and 3 confirmed; Risk 2 not yet assessed

posterior_samples <- cost_post_pdf(

num_sims = 5000,

observed_risks = observed_risks,

means_given_risks = means_given_risks,

sds_given_risks = sds_given_risks,

base_cost = base_cost

)Prior vs. Posterior Cost Distribution

Plotting both distributions on the same axes shows how the evidence shifts the cost estimate:

xlim_range <- range(c(prior_samples, posterior_samples))

# Prior cost histogram

hist(prior_samples,

breaks = 40, freq = FALSE,

col = rgb(0.27, 0.51, 0.71, 0.5), # steelblue, semi-transparent

border = "white",

xlim = xlim_range,

main = "Prior vs. Posterior Cost Distribution",

xlab = "Total Cost ($)",

ylab = "Density"

)

# Posterior cost histogram (overlaid)

hist(posterior_samples,

breaks = 40, freq = FALSE,

col = rgb(0.84, 0.24, 0.31, 0.5), # tomato, semi-transparent

border = "white",

add = TRUE

)

abline(v = mean(prior_samples), col = "steelblue", lty = 2, lwd = 2)

abline(v = mean(posterior_samples), col = "tomato", lty = 2, lwd = 2)

legend("topright",

legend = c(

paste0("Prior (mean = $", format(round(mean(prior_samples)), big.mark = ",")),

paste0("Posterior (mean = $", format(round(mean(posterior_samples)), big.mark = ","))

),

fill = c(rgb(0.27, 0.51, 0.71, 0.5), rgb(0.84, 0.24, 0.31, 0.5)),

bty = "n"

)

Interpretation: The posterior distribution is narrower and shifted, observing which risks materialized eliminates uncertainty about some cost components. The remaining spread reflects uncertainty from unobserved risks and cost variability in the confirmed risks.

Summary

The Bayesian workflow in PRA follows a natural before-and-after structure:

-

Before observations — use

risk_prob()andcost_pdf()to characterize the risk landscape. -

As evidence arrives — use

risk_post_prob()andcost_post_pdf()to update estimates. -

NA values in

observed_causesandobserved_risksrepresent causes/risks that have not yet been assessed; they are correctly excluded from the Bayesian update.

This approach is particularly powerful in phased projects where information about risk drivers becomes available progressively, allowing cost forecasts to be refined at each stage.