The Second Moment Method (SMM) is a fast, analytical alternative to Monte Carlo simulation for estimating project cost or schedule uncertainty. Rather than running thousands of iterations, SMM propagates uncertainty through a project mathematically using only the mean and variance of each task, the “first two moments” of the probability distribution.

When to Use SMM

SMM is best suited for early-stage estimates when:

- Speed matters and simulation run-time is a concern

- You have credible mean and variance estimates for each task

- Tasks are approximately independent or have well-characterized correlations

- You need a quick sensitivity check before committing to a full Monte Carlo run

Method Overview

For a project with n tasks, SMM computes:

- Total mean: Sum of individual task means:

- Total variance: Sum of variances plus twice the sum of all pairwise covariances:

- Covariance: Derived from the correlation matrix:

Example

We analyze a 3-task project with task durations in weeks. Each task has a known mean and variance, and correlations between tasks are provided.

task_means <- c(10, 15, 20) # Expected duration for each task (weeks)

task_vars <- c(4, 9, 16) # Variance of each task duration

cor_mat <- matrix(c(

1.0, 0.5, 0.3,

0.5, 1.0, 0.4,

0.3, 0.4, 1.0

), nrow = 3, byrow = TRUE)

result <- smm(task_means, task_vars, cor_mat)

cat("Total Mean Duration: ", round(result$total_mean, 2), "weeks\n")Total Mean Duration: 45 weeks

Total Variance: 49.4

Total Std Deviation: 7.03 weeks

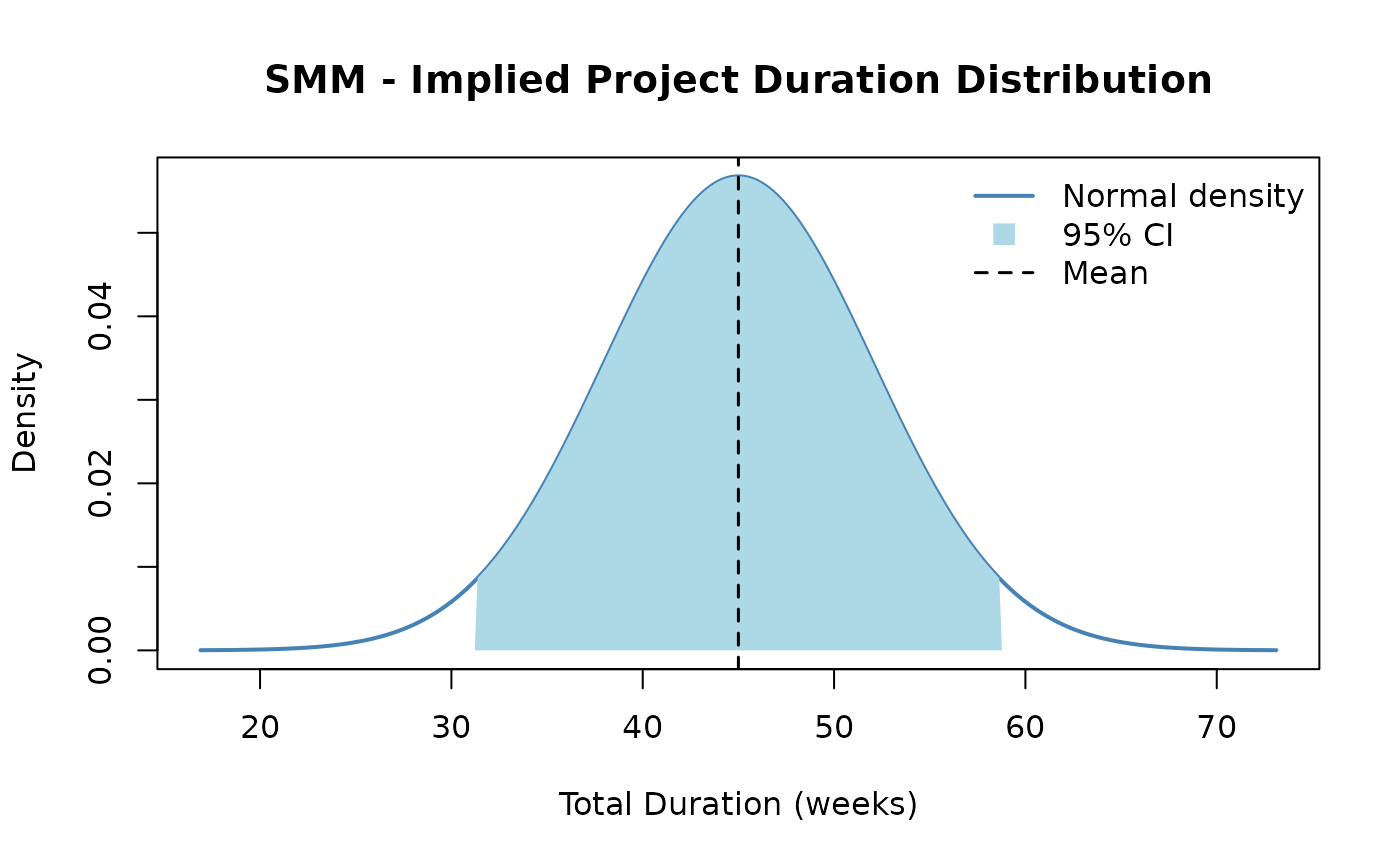

Implied Distribution and Confidence Interval

SMM assumes the total project duration is approximately normally distributed. This allows us to construct a confidence interval directly from the mean and standard deviation.

A 95% confidence interval for total project duration is approximately:

total_mean <- result$total_mean

total_sd <- result$total_std

ci_lower <- total_mean - 1.96 * total_sd

ci_upper <- total_mean + 1.96 * total_sd

cat("95% CI: [", round(ci_lower, 1), ",", round(ci_upper, 1), "] weeks\n")95% CI: [ 31.2 , 58.8 ] weeks

The plot below shows the implied normal distribution of total project duration:

x_range <- seq(total_mean - 4 * total_sd, total_mean + 4 * total_sd, length.out = 300)

y_range <- dnorm(x_range, mean = total_mean, sd = total_sd)

plot(x_range, y_range,

type = "l", lwd = 2, col = "steelblue",

main = "SMM - Implied Project Duration Distribution",

xlab = "Total Duration (weeks)", ylab = "Density"

)

# Shade 95% CI region

x_ci <- x_range[x_range >= ci_lower & x_range <= ci_upper]

y_ci <- dnorm(x_ci, mean = total_mean, sd = total_sd)

polygon(c(ci_lower, x_ci, ci_upper), c(0, y_ci, 0),

col = "lightblue", border = NA

)

abline(v = total_mean, col = "black", lty = 2, lwd = 1.5)

legend("topright",

legend = c("Normal density", "95% CI", "Mean"),

col = c("steelblue", "lightblue", "black"),

lty = c(1, NA, 2), lwd = c(2, NA, 1.5),

pch = c(NA, 15, NA), pt.cex = 1.5,

bty = "n"

)

Comparison with Monte Carlo Simulation

Running Monte Carlo simulation with the same task distributions (and no correlation, for a clean comparison) validates the SMM mean. The two methods should yield very similar total means; differences in variance arise because SMM and MCS handle correlated sampling differently.

# Represent each task as a normal distribution for MCS comparison (independent case)

task_dists_for_mcs <- list(

list(type = "normal", mean = task_means[1], sd = sqrt(task_vars[1])),

list(type = "normal", mean = task_means[2], sd = sqrt(task_vars[2])),

list(type = "normal", mean = task_means[3], sd = sqrt(task_vars[3]))

)

# Run MCS without correlation (identity = fully independent)

mcs_result <- mcs(10000, task_dists_for_mcs)

# SMM variance without correlation = sum of individual variances

smm_var_nocor <- sum(task_vars)

comparison <- data.frame(

Method = c("SMM (independent)", "Monte Carlo (10,000 runs)"),

Total_Mean = round(c(result$total_mean, mcs_result$total_mean), 2),

Total_Variance = round(c(smm_var_nocor, mcs_result$total_variance), 2),

Total_StdDev = round(c(sqrt(smm_var_nocor), mcs_result$total_sd), 2)

)

knitr::kable(comparison, caption = "SMM vs. Monte Carlo Comparison (independent tasks)")| Method | Total_Mean | Total_Variance | Total_StdDev |

|---|---|---|---|

| SMM (independent) | 45.00 | 29.00 | 5.39 |

| Monte Carlo (10,000 runs) | 45.01 | 29.83 | 5.46 |

The two methods agree closely on the mean and variance. SMM is faster but assumes normality; Monte Carlo is more flexible and can use any distribution type. When tasks are correlated, SMM adds covariance terms analytically while MCS uses a correlation-based sampling scheme.

Benefits and Limitations

| SMM | Monte Carlo | |

|---|---|---|

| Speed | Instant (analytical) | Slow (thousands of iterations) |

| Inputs needed | Mean + variance per task | Full distribution per task |

| Distribution assumption | Normal (by Central Limit Theorem) | Any distribution |

| Correlation handling | Explicit covariance formula | Cholesky decomposition |

| Skewness / tails | Ignored | Captured accurately |

| Best for | Early estimates, quick checks | Detailed risk analysis, non-normal tasks |